- Created by admin, last modified by AdrianC on Apr 01, 2016

This information applies to MYOB AccountRight version 19. For later versions, see our help centre.

https://help.myob.com/wiki/x/bQGc

Answer ID:9172

Periodical inventory is a system of accounting for inventory where the goods on hand are only determined by a physical count.

Unlike perpetual inventory systems, where inventory updates are made on a continuous basis, periodical inventory might be useful if you maintain minimal amounts of inventory and a physical inventory count is easy to complete.

Before implementing periodical inventory, you should discuss its suitability with your accounting advisor.

Using the periodical inventory system, when stock is purchased it's immediately expensed to a cost of sales account. When stock is sold, there is no entry to cost of sales. In order to be able to report the value of stock you have on hand, end of period journals must be recorded.

Here are two methods you can use based on how much detail you want to show in the cost of sales section of your Profit & Loss Statement.

- Create two accounts. For details on creating accounts, see the AccountRight help (Australia | New Zealand):

- a Stock On Hand (Asset) account

- a Purchases (Cost of Sales) account

- Set up your inventory items:

- select the options I BuyThis Item and I Sell This Item.

- for the Expense Account for Tracking Costs select the Purchases (Cost of Sales) account.

Select a relevant Income Account for Tracking Sales. Here's our example:

The I Inventory This Item option should never be selected when using this method.

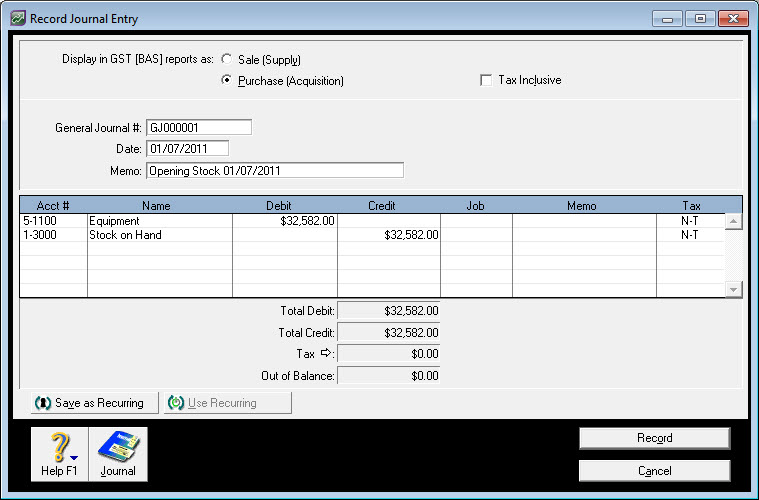

- At the beginning of the financial year, if there's a balance in the Stock On Hand account you need to prepare a journal entry:

- debit the Purchases (Cost of Sales) account

- credit the Stock On Hand (Asset) account

- the amount entered needs to be the value of the Stock on Hand as at the end of the previous financial year Here's our example:

The effect of the general journal entry will leave the account with a zero balance.

- At the end of the financial reporting period, make an adjustment to the Purchases (Cost of Sales) account to reflect the value of stock still on hand.

- Perform a stocktake and accurately value the stock on hand at the end of the financial reporting period.

- Prepare a journal entryto reflect the value of stock counted in the stocktake:

- debit the Stock on Hand (Asset) account

- credit the Purchases (Cost of Sales) account

- the amount entered should be the value determined in the stocktake. Here's our example:

- Print the Profit & Loss Statement and Balance Sheet reports.

- On the first day of the next financial period, prepare a journal entry to reverse the effects of the closing stock adjustment.

- debit the Purchases (Cost of Sales) account

- credit the Stock on Hand (Asset) account

- the amount entered should be for the same value entered in Step 4.

After the journal entry has been performed, the Stock on Hand (Asset) account should be returned to a $0 balance. At the end of future financial reporting periods, repeat Steps 4 and 5 to accurately reflect the true Cost of Sales figure in your Profit & Loss Statement and show the value of stock on hand in the Balance Sheet.

- Create the following accounts. For details on creating accounts, see the AccountRight help (Australia | New Zealand):

- Opening Stock (Cost of Sales)

- Closing Stock (Cost of Sales)

- Purchases (Cost of Sales)

- Stock on Hand (Asset) account

- Set up your inventory items:

- select the options I Buy This Item and I Sell This Item

- for the Expense Account for Tracking Costs select the Purchases (Cost of Sales) account

- select a relevant Income Account for Tracking Sales

- At the beginning of the financial year, prepare a journal entry to show the Opening Stock balance in the Profit and Loss statement:

- debit the Opening Stock (Cost of Sales) account

- credit the Stock on Hand (Asset) account

- the amount entered should be the value shown as Stock on Hand in the Balance Sheet. Here's our example:

- During the month, record your purchases and sales as per usual. Make sure that the allocation account used for Service purchases is the Purchases (Cost of Sales) account.

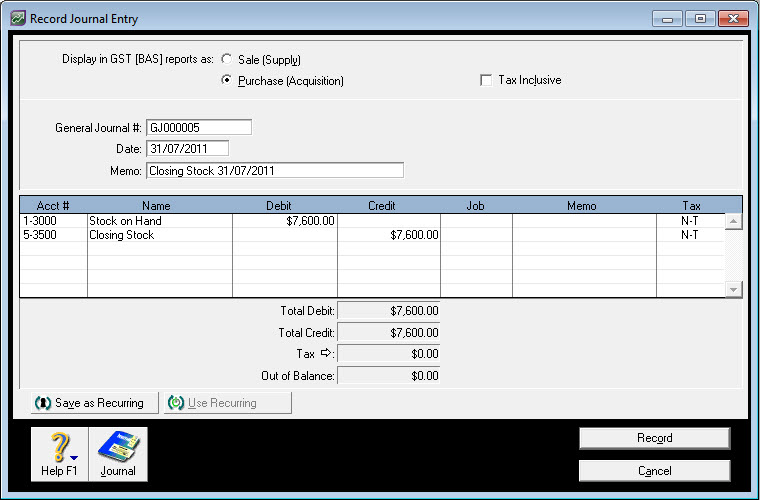

- On the last day of the month, perform a stocktake and value your stock on hand and prepare a journal entry to record this:

- debit the Stock on Hand (Asset) account

- credit the Closing Stock (Cost of Sales) account

- the amount entered should be the value determined in your stocktake. Here's our example:

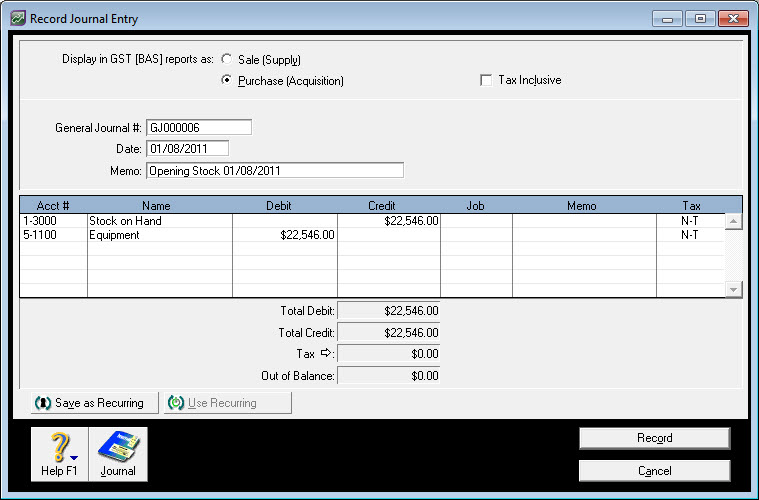

- On the first day of the next month, prepare a journal entry to reverse the closing stock entry:

- debit the Opening Stock (Cost of Sales) account

- credit the Stock on Hand (Asset) account

- the amount entered should be the previous month's closing stock value. Here's our example:

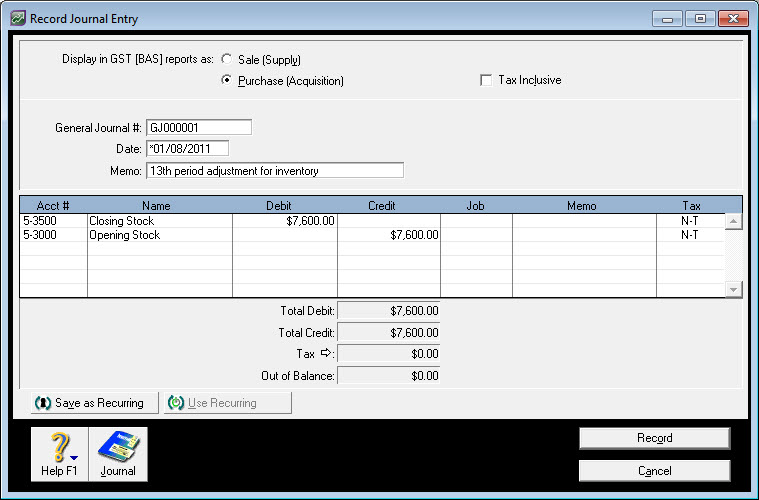

- Enter a year-end adjustment to reverse the impact on the opening stock and closing stock expense accounts.

- add an asterisk in front of the date to allocate the transaction to the 13th period

- debit the Closing Stock (Cost of Sales) account

- credit the Opening Stock (Cost of Sales) account

the amount entered should be the same amount as entered in steps 5 and 6 Here's our example:

If this journal entry isn't recorded, the opening and closing stock will increase every time you enter an end of month journal.