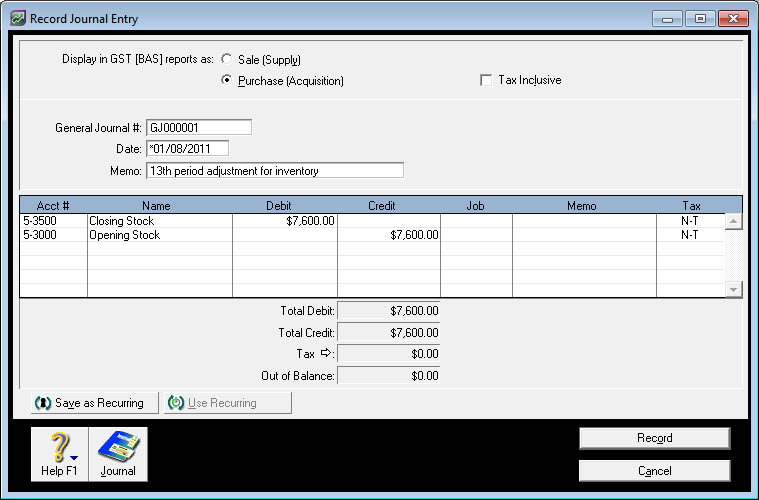

Answer ID:9172Periodical inventory is a system of accounting for inventory where the goods on hand are only determined by a physical count. Unlike perpetual inventory systems, where inventory updates are made on a continuous basis, periodical inventory might be useful if you maintain minimal amounts of inventory and a physical inventory count is easy to complete. Before implementing periodical inventory, you should discuss its suitability with your accounting advisor. Using the periodical inventory system, when stock is purchased it's immediately expensed to a cost of sales account. When stock is sold, there is no entry to cost of sales. In order to be able to report the value of stock you have on hand, end of period journals must be recorded. Here are two methods you can use based on how much detail you want to show in the cost of sales section of your Profit & Loss Statement. |