How satisfied are you with our online help?*

Just these help pages, not phone support or the product itself

Why did you give this rating?

Anything else you want to tell us about the help?

What is each ATO reporting category for?

Use this information to work out which reporting categories you need to assign to your pay items. The STP Phase 2 reporting categories can be assigned now but they won't apply until STP Phase 2 begins.

| ATO reporting category (Phase 1) | ATO reporting category (Phase 2) | More information | ATO links |

|---|---|---|---|

| Gross Payments | Gross payments | Include pay items you use for paying salary and wages. For STP Phase 1, this includes:

For STP Phase 2, payments that don’t sit into any of the main categories, assign them to Gross payments (but check this with the ATO). | The rules of reporting through Single Touch Payroll |

Allowance - Car | Allowance - cents per km | This includes payments you make to cover your employees’ work-related expenses. For allowances that don’t sit into any of the main categories, assign them to Allowance – Other (but check this with the ATO). Typically, you wouldn't include amounts you pay for living-away-from-home allowance because these amounts are not assessable income (but check this with the ATO). | |

Lump Sum A - Termination | Lump Sum A - Termination | Lump sum payments, typically paid as employment termination payments, may include:

See the FAQs below for details on each lump sum payment type. For STP Phase 2: Lump Sum W has been added which is for return to work payments. Lump Sum E payments work differently for STP Phase 2. Tell me more Lump sum payments are a complex area. Chat to your advisor or check with the ATO for more guidance. | |

CDEP Payments | CDEP Payments | Assign pay items for:

| CDEP payments |

| Exempt Foreign Income | Exempt Foreign Income | This could be assigned to pay items such as salary, wages, commissions, bonuses and allowances that are exempt from Australian tax. | Exempt foreign employment income |

| ETP - Taxable component ETP - Tax free component | ETP - Taxable component ETP - Tax free component | These are pay items used to track the taxable and tax-free components of employment termination payments. ETPs are concessionally taxed up to a certain limit, or 'cap'. Certain types of termination payments are tax free up to a certain limit, for example, if the ETP is because of redundancy or early retirement. | Taxation of termination payments |

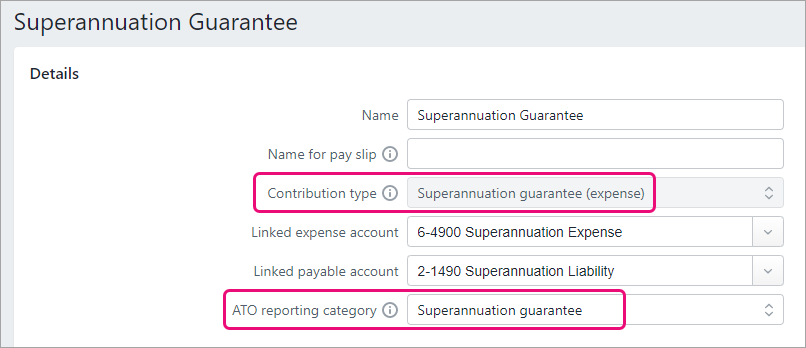

The ATO Reporting Category is automatically assigned for superannuation pay items set up with the following Contribution Types :

- Superannuation Guarantee (expense)

- Employee Additional (deduction)

- Redundancy (expense)

- Spouse (deduction)

| ATO reporting category (Phase 1) | ATO reporting category (Phase 2) | More information |

|---|---|---|

Superannuation Guarantee | Superannuation Guarantee | This information is reported to the ATO to ensure that employee super funds are receiving the correct amounts. |

| Reportable Employer Super Contributions | Reportable Employer Super Contributions | Use this to assign superannuation pay items which handle 'reportable' superannuation payments (as classified by the ATO guidelines). Note that this option only appears for Employer Additional (expense), and Salary Sacrifice (deduction) contribution types. |

Salary Sacrifice | Use this to assign salary sacrifice super pay items. |

| ATO reporting category (Phase 1) | ATO reporting category (Phase 2) | Description | ATO reference |

|---|---|---|---|

Deduction - Work Place Giving | Deduction - Work Place Giving | Assign pay items that are donations made under a workplace giving arrangement. | Workplace giving programs |

Deduction - Union/Professional Assoc Fees | Deduction - Union/Professional Assoc Fees | This might include pay items for:

| Union fees, subscriptions to associations and bargaining agents fees |

| ETP - Tax Withholding | ETP - Tax Withholding | Use this reporting category when an employment termination payment has been made to an employee. | Taxation of termination payments |

Salary sacrifice - other employee benefits | For deductions that are for benefits from an effective salary sacrifice arrangement, including those exempt from FBT. | Salary sacrifice arrangements | |

| Not Reportable | All other deductions are usually considered not reportable. This includes things like loan or car payments. This is because they may not need to be itemised on an employee's tax return. If you're not sure if a deduction is reportable, check with your accounting advisor or the ATO. |

The ATO Reporting Category is automatically assigned for the PAYG Withholding pay item.

| ATO reporting category | Old Payment Summary field name | More information |

|---|---|---|

PAYG Withholding | Total Tax Withheld | This is automatically assigned and can't be changed. |

This category reports all tax withheld from the employee, including any extra PAYG that may be deducted.

Assigning ATO reporting categories

You need to assign ATO reporting categories to all pay items you've used in the current payroll year, and whenever you create a new pay items.

If you're setting up STP for the first time, your MYOB business is checked to find any pay items that don't have an ATO reporting category assigned—so you can then assign one. You can also manually check your pay items and, if required, assign an ATO reporting category.

If you'd like to start assigning ATO reporting categories in preparation for STP Phase 2, you (or your bookkeeper) can do so within each pay item.

The current (Phase 1) ATO reporting categories will apply until STP Phase 2 starts. But if you'd like to get a head start, you can assign the updated ATO reporting categories now.

If you need help choosing, check the info above or speak to your accounting advisor or the ATO.

- Go to the Payroll menu and choose Pay items.

- Click the Wages and salary, Superannuation or Deductions tab.

- Choose the applicable ATO reporting category (STP Phase 2).

- Click Save.

- Repeat for each of your wage, super and deduction pay items.

Yes

Yes

No

No

Thanks for your feedback.

Thanks for your feedback.